Beneath the Shingles: The Viability in Developing Attainable Housing

By Dave Armanetti, Director of Real Estate Development

April 2026

When I joined the Housing Nantucket team in Fall 2025, after more than a decade managing permitting, development, and construction projects on Nantucket, one of my first tasks was revisiting the financial models used to determine whether a housing project is feasible. At its core, project viability depends on three key factors: rental income, construction costs, and financing costs, driven largely by interest rates.

As I updated these calculations, I found myself comparing current numbers to project budgets from 2019. At the time, those projects felt expensive and difficult to finance. Looking back now, they almost seem unrealistic by comparison.

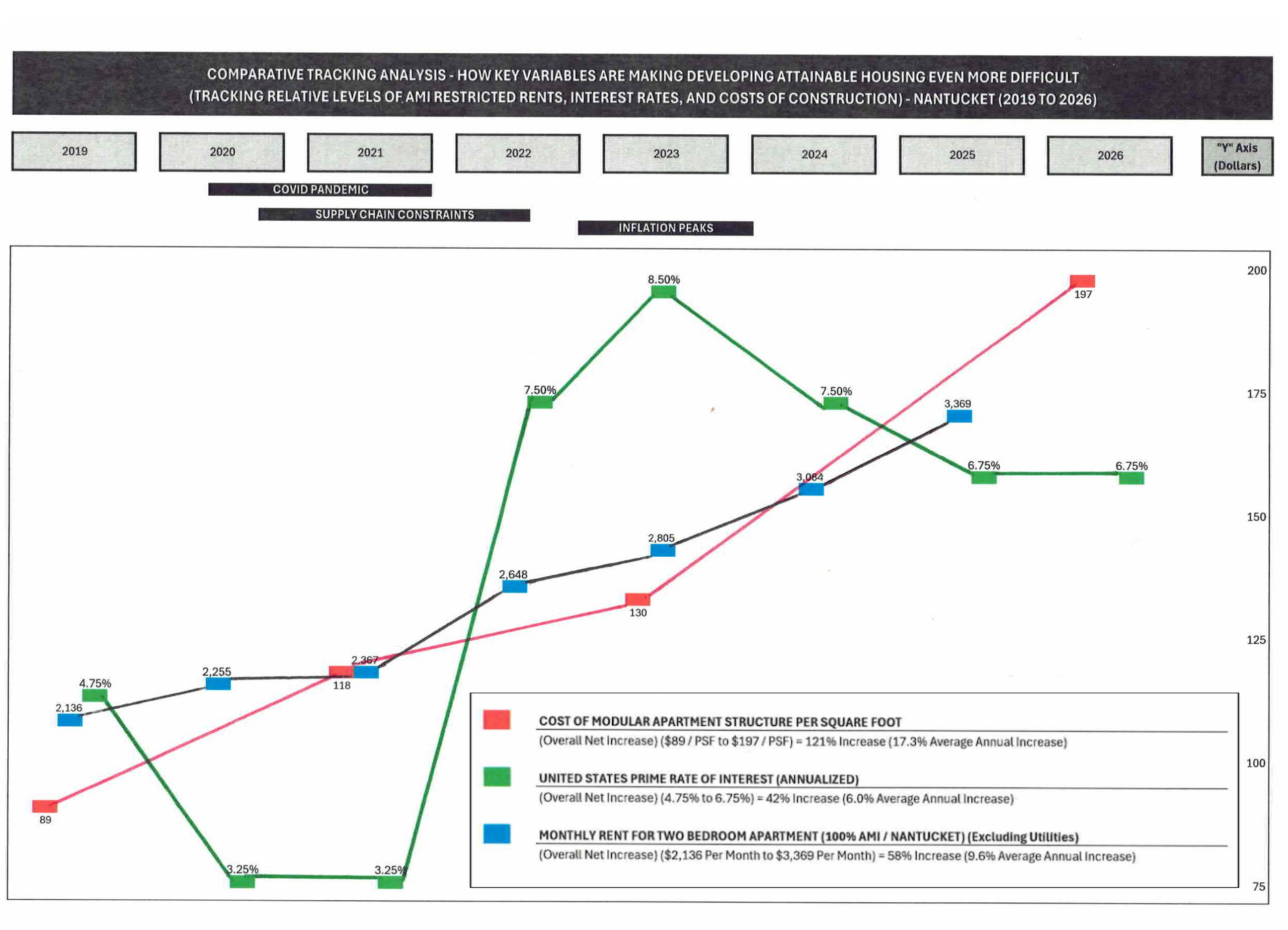

In 2019, the cost of a modular apartment structure was under $90 per square foot before transportation to Nantucket. Today, that same cost is approaching $200 per square foot – more than double – and that figure still does not include transporting the modules to the island, foundations, or the remaining on-island construction work required to complete the building.

That single comparison tells a much larger story about what has happened to housing development over the last six or seven years.

At Housing Nantucket, we describe ourselves as a Community Development Partner because our work extends far beyond simply building housing units. Community development means understanding the broader factors, economic pressures, and long-term challenges shaping whether year-round residents can continue to live and work here. This includes taking into account and appreciating the “human” side of what is otherwise seen as “just math”.

And right now, one of the biggest challenges facing communities everywhere, especially Nantucket, is the widening gap between what housing costs to build and what hard-working people can afford to pay.

We recently put together a graph tracking the three primary variables, first described above, that ultimately determine whether attainable housing projects are financially viable:

- Construction costs (of Modular Apartment Structures) (red)

- Financing costs (Interest Rates) (green)

- Revenue (Monthly AMI-restricted Rents) (blue)

The graph spans the period from 2019 to today, back through the COVID pandemic, the subsequent supply chain crisis, and inflation peaks, and into the current economic environment. And while every developer, contractor, lender, and nonprofit housing organization has felt and understands these shifts and correlations intuitively, seeing all three variables in sharp focus, intersecting together on one chart, is striking.

The pattern is impossible to ignore.

Construction costs have climbed in what is essentially a near-continuous upward trajectory (what are commonly and colloquially referred to as multiple “hockey sticks”). There were initial spikes during COVID, as supply chains broke down and shortages of materials and commodities required for construction spread across the country. These radical costs flattened out, however, albeit slightly, for a short period afterward, but only briefly. Since mid-2023, they’ve accelerated sharply again.

Overall, construction costs, illustrated most specifically herein with the example of the cost per square foot of a modular apartment building structure, but across the board, for stick-built (traditionally constructed) buildings, and including components like site work, foundations, general contractor costs, and subcontractor costs, have all increased, unabated, by a factor of between 100% to 150% (cumulatively) since 2019, an average increase of roughly 15% to 20% (per year).

At the same time, interest rates have moved to further exacerbate the challenge. During COVID, rates dropped dramatically, but only very temporarily, creating a short sense of relief and liquidity in the market – but this occurred simultaneously with the worldwide COVID pandemic, when most economic activity (including new housing development and construction) screeched to a halt. Prime lending rates fell from 4.75% to 3.25%, but very few projects were able to move forward during that span.

Then inflation hit.

In only about 18 months, from 2022 to mid-2023 rates surged to 8.5%. Even though they’ve moderated somewhat since then, today’s borrowing environment remains dramatically more difficult than it was several years ago. And it’s not just the rates themselves. Lending standards have become considerably more restrictive, as well. Minimum debt service coverage requirements have increased. Maximum loan-to-cost and loan-to-value ratios have compressed. Equity requirements are larger. Financing has become materially harder to secure, and much more expensive.

Investors, even community-minded and philanthropically-generous investors, of which we are very fortunate to have the support from so many of here at Housing Nantucket, have a myriad of other deserving organizations to support, and many other sources where they can earn higher returns on their investment (which they are sometimes contractually bound to do under their charters and bylaws).

Meanwhile, rents, even restricted workforce housing rents tied to AMI calculations, have risen steadily over the same period. A two-bedroom unit restricted at 100% AMI on Nantucket increased from roughly $2,136 per month in 2019 to approximately $3,369 today.

That sounds significant, because it is. But it still hasn’t come close to keeping pace with construction costs.

Rents have increased by about 58% during this same timeframe. Construction costs have increased by more than double that amount.

That widening gap of viability for workforce housing projects, even when they are efficiently managed, and even when they benefit from the largess of the community which has repeatedly shown strong political will and generosity in approving economic support (subsidy) from the Town of Nantucket, that are so critical to the health of the underlying economy and the quality of life on Nantucket, is really the story here.

And operating expenses, insurance, utilities, trash removal, maintenance, compliance, labor, have also all increased substantially as well, further eroding project feasibility.

The result is that projects which might have “penciled” even somewhat comfortably, six or seven years ago, now require multiple sources and layers of subsidies, additional equity, philanthropic support, public-private partnerships, or significantly more creative financing structures simply to become feasible.

This is not unique to Nantucket. It’s happening everywhere.

But on Nantucket, where logistical costs, labor shortages, transportation constraints, land availability, and extraordinarily high land prices already create an unusually difficult development environment, the impacts are amplified.

One of the reasons I wanted to share this graph and accompanying story publicly is because conversations around housing often become oversimplified. People understandably ask: “If rents are so high, why isn’t more housing being built to meet demand?”

The multiple, interrelated reasons outlined above is why.

The economics determining the viability of housing development have fundamentally shifted over the last several years. Construction costs have risen at nearly three times the rate of rents, while financing costs and operating costs have also moved sharply upward.

The “math” simply works differently than it did before, and not in a favorable way.

That reality is also why the role of a true community development partner matters more than ever. Solving workforce housing challenges today requires more than building structures. It requires long-term planning, creative financing, collaboration with public and private partners, community engagement, and the ability to navigate increasingly difficult economic conditions while keeping the focus on year-round residents.

And despite these challenges, the need for workforce housing has only become more urgent. Which means we all have to continue finding ways to bridge a gap that keeps getting wider, together. Because if we don’t, the market alone, despite all the incredible effort that has been made by Town Meeting voters, the many dedicated Town officials and Town staff, and all the other organizations and stakeholders (including all of the many talented and committed local design and engineering professionals, suppliers, contractors, and subcontractors) who work collaboratively and tirelessly every day with us to further attack this challenge, will not solve this problem.

Despite these constraints and increasing challenges, I am ever optimistic and confident that all these myriad challenges can be overcome, and that we will continue to work together to make progress in creating more units and types of suitable housing, and to strive to continue to improve the quality of life of the incredibly unique community that we all love and benefit from.